With opportunities in the young population, widening middle class, development in telecoms and exodus of people in Africa, foreign reinsurers that once chided the continent are swarming for businesses on the continent with confidence in consumers with throwaway incomes and hefty infrastructure schemes being built, Odimegwu Onwumere writes

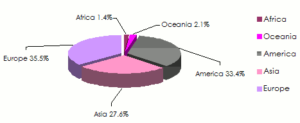

Over the years, the West was seen as a place for mature reinsurance business with expensive and classy competition. For example, Europe spawned $1.69bn premium in 2014, something stakeholders said was in the ratio of 35.53 per cent allocation of the world insurance market. The whistle-blower, Sigma 2014 World Insurance Report by Swiss Re, expressed that the sum threw in 6.83 per cent to the Gross Domestic Product (GDP). In that index, Africa recorded about $68.97m, which was regarded as the lowest among the committee of nations and diffused to 1.44 per cent share of the global insurance market. But this trend may be no more as the reinsurance markets on the continent are expected to gain from strapping underlying growth, with insurance premiums of US$ 64 billion in 2016, as according to Africa Reinsurance Pulse at the 21st African Reinsurance Forum in Dakar, Senegal; and there has been a drive in the escalation of the primary markets.

In its Q3 2016, Continental Reinsurance, an amalgamated reinsurer, scripting business in over 50 countries across the African continent announced that it made 16% growth in gross premium income of N17.5billion, as against N15.1 billion in 2015. This juxtaposed to what Sigma further exposed, saying that $1.59bn premium was gained by America and $1.31bn premium or about 27.57 per cent share of the global market was attained by Asia in 2014, but the 2016 indicator expressing US$64 billion for reinsurers in Africa, has shown that reinsurance markets on the continent are really making headway in adding to Africa’s GDP. Africa has a great hope because of the diversity in the African reinsurance markets, given their regional sub-sets and the continent can boast of about 35 registered reinsurers operating on ground. Unlike when the continent had a decline in life insurance from 6% in 2013 down to 1.6% in 2014 and non life insurance taking the same method from 4.4% in 2013 to 1.8% in 2014, the trend can be seen is changing with the continent regarded as the most vigorous continent for business in the world.

There are records showing that Africa has recorded USD $2 trillion on her economic stage. AM Best, an international rating agency would attest to the fact that by 2020, Africa might have $2.6 trillion USD in its GDP. It’s expected, according to World Bank that by 2025, many countries in Africa will rise to the “middle income” position. The manifest is that time was gone when African countries were wearing diapers in the reinsurance markets. South Africa was however excluded then and was regarded as one of Africa’s most advanced in the sector. In those years, reinsurance markets on the continent had extremely low capital base, except 2013 Swiss Re report, surmising that South Africa earned 75 percent, or $51.6bn, of all insurance premiums in Africa, while foreign firms in the Americas, Europe and Asia superintended 75 per cent of reinsurance deals in Africa.

There are records showing that Africa has recorded USD $2 trillion on her economic stage. AM Best, an international rating agency would attest to the fact that by 2020, Africa might have $2.6 trillion USD in its GDP. It’s expected, according to World Bank that by 2025, many countries in Africa will rise to the “middle income” position. The manifest is that time was gone when African countries were wearing diapers in the reinsurance markets. South Africa was however excluded then and was regarded as one of Africa’s most advanced in the sector. In those years, reinsurance markets on the continent had extremely low capital base, except 2013 Swiss Re report, surmising that South Africa earned 75 percent, or $51.6bn, of all insurance premiums in Africa, while foreign firms in the Americas, Europe and Asia superintended 75 per cent of reinsurance deals in Africa.

Alluring And Dynamic

In spite of the competition and new investors besieging for business in Africa, African reinsurers have made their mode of operations insufficient and underused hence creating room for foreigners to invest on the continent and making the continent a potential market. There are cases of inept capacities of regional players and incompetent underwriting and risk management staff.

Despite some wavering economic policies in some countries of Africa today and the many years of neglect meted out to the reinsurance markets in Africa by American and European reinsurers, the sector is becoming alluring and dynamic, because of unswerving GDP growth and the Western firms beginning to gear up for business on the continent, but especially in Sub-Sahara Africa (SSA).

Checks have revealed inter alia that France’s leading insurer, AXA in February 2016 had informed of its decision to spend €75m ($87.27m) in Africa Internet Group (AIG), according Jean-Baptiste Mounier, media relations officer at AXA Group. Buttressing the point, Mounier revealed, “Market growth has been boosted by government reforms such as mandatory motor and group life insurance.”

The source further highlighted that the coming of AXA Group, was intended to provide for insurance products and services through Jumia – Nigerian online vendor with warehouses across the country, and other AIG podiums transversely in Africa.

Conversely, before this development, stakeholders in the field had singled Nigeria out (apart from South Africa?) as the only country with a rationally large capital whereas other countries had low capital prerequisite, thereby triggering the anxiety in reinsurers not to agree to big ticket risks, hence many of the businesses from the continent went offshore.

Capital Flight & Cession

Over 75% of African reinsurance market was lost to assets flight, said the Group Managing Director, Africa Reinsurance Corporation, Cornellie Karekezi. Supporting the argument, those who know better explained that the loss was as a result that 75% of the market share was located outside the continent.

Over 75% of African reinsurance market was lost to assets flight, said the Group Managing Director, Africa Reinsurance Corporation, Cornellie Karekezi. Supporting the argument, those who know better explained that the loss was as a result that 75% of the market share was located outside the continent.

But experts’ outlook was, “In order to protect their national market, many African countries limit access to reinsurance for foreign companies. A compulsory cession to the national reinsurer is oftentimes imposed on insurers. Moreover, equally compulsory cessions are added to other reinsurers or entities (specialized pools) in which the State possesses interests.

“For instance, in Senegal, local insurance companies are required to cede to the national reinsurer a fixed percentage over all policies written nationwide. To this “baseline” or on ground-up basis cession another cession on reinsurance treaties is added.

“Besides, regional reinsurer CICA-Re and continental reinsurer – Africa Re, also benefit from compulsory cessions. The same scheme, with some variables (ground up cessions+reinsurance cession or reinsurance cession only) exists in Ghana, Nigeria, Kenya, Gabon, Algeria, Morocco, Egypt…”

Massive Potentials

A leading market broadsheet in Kenya had a luring caption – Africa’s insurance market a ‘giant waking up’ – on its June 27, 2016 edition. Not many perhaps reasoned deeply the prophetic message that the paper was intended to pass.

The message could be likened to an Ernst & Young report, “Africa, with a median age of 20 years, is the youngest continent. Its population amounted to 1.138 billion people in 2014 but it is poised to double in the course of the next 40 years to reach nearly 2 billion people, that is 20% of the global population in 2050. African labour is therefore poised to reach 1.1 billion people by 2040, a figure above labour projections for China and India.”

But here is the source in Nairobi explaining, “When KPMG, the advisory company, held its inaugural East Africa Insurance Conference in February, organisers were surprised that more than 100 industry participants attended. James Norman, KPMG’s regional insurance head, was equally enthused when a similar number attended the launch of a report on the sector last week.”

Quoting James Norman, KPMG’s regional insurance head, the source added, “There’s a real buzz about the sector because opportunities are immense. There’s a young population, a growing middle class – most with smartphones – and an increasingly large diaspora coming back. There’s a whole new generation of savvy consumers with disposable incomes and large infrastructure projects being built.”

Fastest Growing

There have been fingers suggesting that with the lack of insurance when countries on the continent like Mozambique, Kenya, Tanzania, South Africa, and Nigeria, experienced severe draught and extensive flooding, showed that Africa is a potential industry for the re/insurance markets.

The 2016 South African Insurance Survey homepage examined, “Rating agencies are awarding stronger ratings to African Reinsurance providers despite the continuing economic crisis in the West.”

The highlight of this is that Kenya, Nigeria and Morocco are among the fastest growing re/insurance markets in Africa, said Dr. Schanz, Alms & Company in its annual review (Africa Reinsurance Pulse 2016).

The revelation further pointed to the fact that these countries are driven by the size and multiplicity of their economies, a juvenile and getting-bigger population and intricate dogmatic regimes.

Recorded Gains

Investigations have revealed that premiums totaling US$ 43.7 billion were recorded in African life insurance in 2015, something that was double the dimension of the non-life insurance market (US$ 20.4 billion). In another angle, it was looked at to be in the ratio of two thirds of the market’s general premium quantity.

A reliable source narrated, “The top 5 life insurance markets of the region are South Africa (US$ 37.5 billion), with a dominating share of 86%, followed by Morocco (US$ 1.1 billion), Egypt (US$ 1.0 billion), Kenya (US$ 0.7 billion) and Namibia (US$ 0.6 billion).

“At a time in 2015, African non-life premiums stood at US$ 20.4 billion, representing about 1% of global non-life premiums. The five largest markets – South Africa, Morocco, Algeria, Kenya and Egypt – account for 68% of the total. In non-life insurance, South Africa’s market share, at 41%, is less dominant than in the life space.”

Very Diverse

On balance, upon that many analysts believe that Africa’s financial and insurance markets are very diverse in the understanding of “socioeconomic indicators, financial literacy”, Magdalena Ramada, who specializes in emerging-market research and multinational company expansion for Willis Towers Watson, a leading voice in insurance markets, explained in a public appearance that SSA alone, has a massive aptitude that makes it “a new frontier in the insurance markets” for lots of insurance transnational. “Here’s why,” explained Ramada:

- SSA accounts for just 2.2% of global GDP. In 2014, GDP growth was 4.6% (5.7% including South Africa), and 2015 growth forecasts are 4.2% (5%).

- With 16% of the world’s population, it is the second-most populous continent, with around 1.1 billion people and an expected population of 2.3 billion by 2050.

- Over 25% of all languages in Africa are only spoken, with over 2,000 recognized languages.

- More than half of the population is under the age of 25.

- Expected economic growth and growing middle classes, technology-enabled distribution channels, a high mobile phone penetration rate and a very low insurance penetration – 3.5% on average for SSA (less than 1% if South Africa is excluded) in a market of 1.1 billion people.

The source orated that with the low penetration of re/insurance on the continent, with an example of “even lower insurance density (US$61)” the figures for SSA become quasi-negligible. But for Delphine Maïdou, CEO of Allianz Global Corporate & Specialty Africa, “Nigeria is Africa’s largest country by gross domestic product and has a mere 0.6 percent insurance penetration. She has all the ingredients for a thriving insurance industry because of its vast population of 170 million and active economy.”

Internal Growth

The economy of the continent skyrocketed in 2002 with the International Monetary Fund (IMF) putting 11 African countries as among countries that are in the echelon of 20 sprinting and enlarging economies by 2017.

The economy of the continent skyrocketed in 2002 with the International Monetary Fund (IMF) putting 11 African countries as among countries that are in the echelon of 20 sprinting and enlarging economies by 2017.

This could be the reason Ramada added, “Demographic and economic growth forecasts estimate that in the next 50 years, Africa will comprise 30% of the world’s population and the region’s consumption will generate internal growth.

“The World Bank classifies half of Africa’s countries as middle income. In fact, Africa’s middle class is growing steadily, having reached the size of India’s middle class, although its geographic dispersion makes it more challenging to leverage.”

In spite of this, Africa Reinsurance had been proud of making 10 per cent of the entire reinsurance market share in Africa quarter of 2016 and there was fear that the company “might not do up to 25 per cent during the period”.

Synergy To Cover Risks

There was apprehension in the dearth of synergy to cover large risks in the areas of oil and energy, and carry on multi-projects and most importantly in the areas of airlines and aviation.

These invariably would make new companies to gain from legal cession. Against this influence, a source by Atlas Magazine, an informant for insurance around the world, had a divergent view as follows:

- That is how in Ghana a third national reinsurer, GN Reinsurance Company, was set up in 2015. As a reminder, Ghanaian insurance companies are not allowed to place their reinsurance on international market unless local capacities have been exhausted.

- In Uganda local insurers are required to cede 15% of their treaties to Uganda National Reinsurance (Uganda Re) set up in 2013.

- In Gabon, the Société Commerciale Gabonaise de Réassurance (SCG-Re) which was established in 2012, benefits from a compulsory cession of 15% of life reinsurance treaties and of 10% of the ones pertaining to the non life reinsurance.

- In Ethiopia, a national reinsurance company – Ethiopian Re – is about to be established. Endowed with 50 million USD in seed capital, the new company’s objective is to increase market capacities.

Heightened Prospect

At the 21st African Reinsurance Forum in Dakar, Senegal, where the Africa Reinsurance Pulse known as the first on the continent was launched, there was heightened prospect in the primary markets with insurance premiums of US$ 64 billion with GDP anticipated to augment by approximately 4% per annum from 2016 – 2020, before the accepted global standard growth rate of 3.6% for the time.

Analysts have said that with the stumpy insurance penetration of 2.9%, as a split of insurance premiums to GDP, there were revelations that the continent had great capability in grabbing with the global middling of 6.23% for 2015.

These were coming when the Africa Reinsurance henchman bared his fears that Africa was competing in capacities and also in ratings, but with minute support from African populaces to help reinsurance and insurance development bolster on the continent.

“More than 90% of Africa’s insurance companies have only been created in the past 40 years. As a result, our industry still has to build the awareness for the benefit of protecting and enabling economic progress…” Corneille Karekedzi said.

Despite that, the Africa Reinsurance that once gasped for breath to control 10 per cent of the entire reinsurance market share in Africa beat its chest that it was controlling 20% of Nigeria’s Reinsurance Market by April 2017.

A delectable Karekezi, said, “Nigeria, where Africa Re is headquartered since 1976, represents an important market for the Corporation as it represents about 13 per cent of its total turnover in 2016.”

The highlight of this is that the continent has been having good news in reinsurance markets lately, not minding the aspersion by Africa Reinsurance clamouring that European and other oversea reinsurers were dominating about 65 percent of the market in Nigeria and the residual 15 percent was divided by other local reinsurers that comprised Continental Reinsurance, and Nigerian Reinsurance.

Odimegwu Onwumere is a Media Consultant based in Rivers State. He contributed this piece via: [email protected] {Graphs sources: Sigma, Swiss Re; Oxford Economics, WIIW, Swiss Re Economic Research & Consulting; Standard Bank, Understanding Africa’s middle class.}

Gabriel Yakubu Aduku, FNIA, PPNIA, OON, AMANA-OGOHI 1- ATA IGALA: A Towering Cypress @80")

{kind=link}